Planning for retirement used to be a daunting task, shrouded in uncertainty and financial stress. But thanks to smart financial tools like the National Pension System (NPS), securing your dream retirement is becoming easier than ever.

The key to unlocking financial freedom in your retirement years lies in starting early. The sooner you plan, the more time your money has to grow through the power of compounding interest. This blog post will equip you with all the knowledge you need to leverage the power of NPS, including scheme preferences and how to get your permanent retirement account number (PRAN), and start paving the path to a fulfilling retirement.

Read more: Start Saving for Your Retirement with NPS

What is NPS and Why Does it Matter?

The NPS scheme is a low-cost retirement and investment product started by the government and regulated by pension fund regulatory and development authority (PFRDA). It is available to all Indian citizens aged 18 to 70 and is an excellent way for individuals to save for their retirement and enjoy tax benefits.

Benefits of NPS

1. Tax benefits

Contributions made towards the NPS scheme qualify for tax deductions under Section 80CCC and 80CCD(1B) of the Income Tax Act. It is a cost-efficient investment that ultimately benefits subscribers. The National Pension Scheme falls into the exempt, exempt, exempt (EEE) category, which implies that contributions, accumulations, and withdrawals are all exempted from taxes.

Know more about the Tax Benefits of NPS at the following links: What are the NPS Tax Benefits Available for Investors?, Best Tax Saving Investment Options for 2024

Here are some of the other advantages of availing the national pension scheme as a retirement pension plan:

2. Returns

NPS offers equity allocation with higher returns than PPF. It has delivered consistent returns of 9-12% over the past decade. Subscribers can change fund managers if they are not satisfied.

3. Risk Assessment

The NPS scheme imposes a cap on equity exposure ranging from 75% to 50%, which decreases by 2.5% annually after the investor turns 50. For investors aged 60 and above, the cap remains fixed at 50% to balance risk and returns and protect the corpus from excessive equity market volatility.

4. Earning Potential

The national pension scheme demonstrates higher earning potential compared to other fixed-income schemes, adding to its attractiveness as a long-term investment option and early retirement scheme. NPS offers a variety of investment options across different asset classes, allowing you to choose a risk-reward profile that aligns with your goals and risk appetite, including bonds by the Government of India.

5. Regulated

Regulated by the pension fund regulatory and development authority (PFRDA), the NPS follows transparent investment norms. Regular performance reviews and monitoring of fund managers by the NPS Trust contribute to a well-regulated and secure investment environment, enhancing the safety of your retirement income and pension account.

6. Flexibility

NPS subscription offers flexibility and adaptability. Contributors can invest at any time, adjust subscription amounts, choose investment options, and manage their accounts online. This enhances convenience and accessibility.

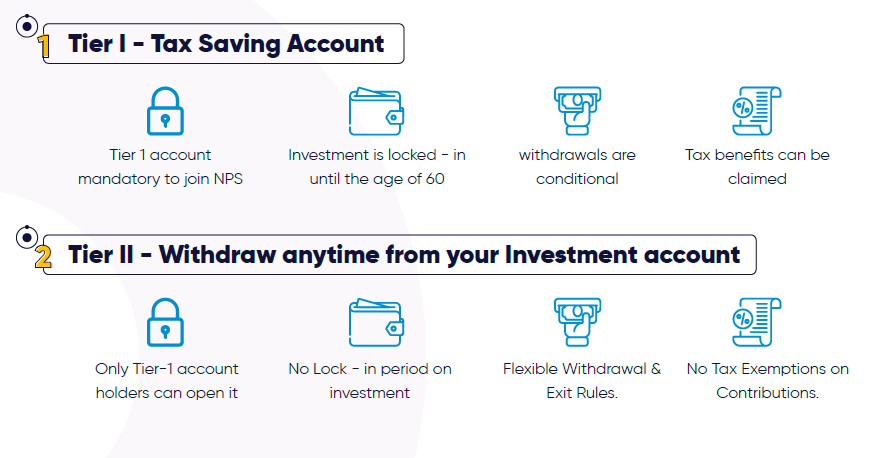

Types of NPS accounts

There are two types of NPS accounts: Tier I and Tier II.

- Tier I account is a mandatory retirement account with restrictions on withdrawals.

- Tier II account is a voluntary retirement account with no restrictions on withdrawals.

Know more: NPS Tier 1 and NPS Tier 2: Which One Is for You?

How to open NPS account

NPS is a great option for individuals who are looking for a long-term investment scheme. Contributions to NPS are tax-deductible with potential to provide good returns over the long term.

Eligibility for NPS

Any Indian citizen between the age of 18 and 70 years can open an NPS account.

NPS Account Opening (Online & Offline)

- You can open an NPS account offline through designated points of presence (POPs) registered with PFRDA. Then fill up a subscriber form and submit it along with your KYC papers. Afterwards, you have to make an initial investment (₹1000 annually). Once you have invested, PoP will then send your Permanent Retirement Account Number (PRAN) in a welcome kit.

- You could also open an NPS account online. To know how to open an NPS account online, click here: NPS Login: How to open an NPS account online?

NPS calculator

Once you have opened your account, you will need to estimate the corpus you need to accumulate for your retirement years. This will depend on various factors including your financial goals and the desired retirement income. An online NPS calculator makes it quite easy to decide your contributions.

This online tool acts as your retirement planning buddy, simplifying the calculations and estimations.

- Your Age: Tell the calculator your current age, like setting the starting point on a map to your retirement destination. This helps it calculate how many years you have to contribute and grow your corpus.

- Investment Amount: Think of the investment amount as the money you're willing to invest now to cover your monthly expenses in the future. It's similar to fueling your retirement vehicle, propelling you towards a secure and fulfilling path.

- Percentage of Annuity: Imagine a steady stream of income after retirement. This percentage determines how much of your total savings you will allocate to buying an annuity, ensuring a steady income in your retirement.

Click here to learn how to Build Your Retirement Corpus using the NPS Calculator

Investment Options and Asset Allocation

Selecting the right fund manager is a crucial step in securing your retirement. Take your time, research thoroughly, and don't hesitate to seek professional advice if needed. Consider these factors when choosing the best pension fund manager for your NPS investment. Read more here - Flexible Contributions and Investment Choices

NPS offers subscribers a high degree of flexibility, including the choice of a pension fund manager and asset allocation. Investors with a higher risk appetite can allocate up to 75% of their funds to equities. This scheme has a proven track record of delivering some of the market's best returns, coupled with tax deduction benefits of upto Rs. 2 lakhs.

Read more at: NPS: Building a Robust Retirement Corpus with Consistency and Stability

NPS Statement Download

As your retirement savings grow, you may find it helpful to download the transaction statement of your NPS account for tax calculation purposes. You have the option to access your annual transaction statements for your NPS Tier 1 account through the Protean CRA website. You can find the steps here: NPS: Contribution, tax details & how to check statement

NPS Withdrawal & Exit

Life throws curveballs, and the NPS is designed to understand such exigencies. In urgent situations, you can access a portion of your retirement savings through the various NPS withdrawal and exit options.

NPS Partial Withdrawal

The National Pension System (NPS) allows participants the flexibility to access a portion of their retirement savings ahead of schedule, subject to specific criteria. Learn more here: NPS Partial Withdrawal Rules

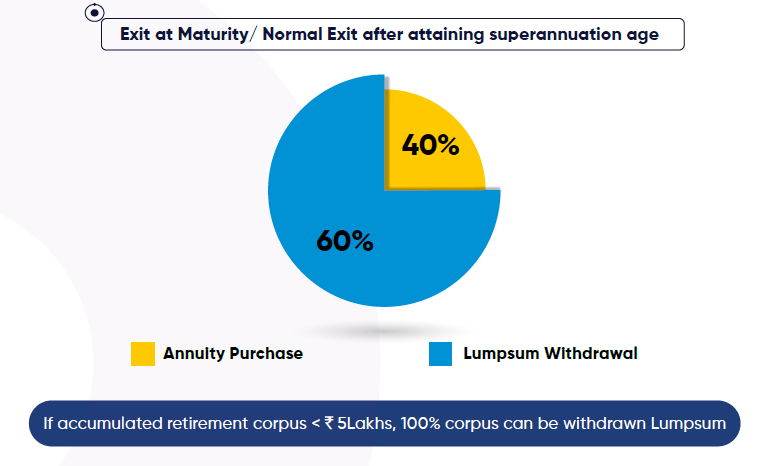

Exit at Maturity

After attaining 60 years of age, upto 60% of the corpus can be withdrawn. Subscriber is mandatorily required to invest minimum 40% of the accumulated NPS corpus (Pension Wealth) for annuity (To know more about the different annuity plans in NPS visit https://cra-nsdl.com/CRAOnline/aspQuote.html). Subscribers can utilise 100% corpus for annuity to receive more pension. If Corpus <5.00 Lakhs, complete withdrawal is permitted.

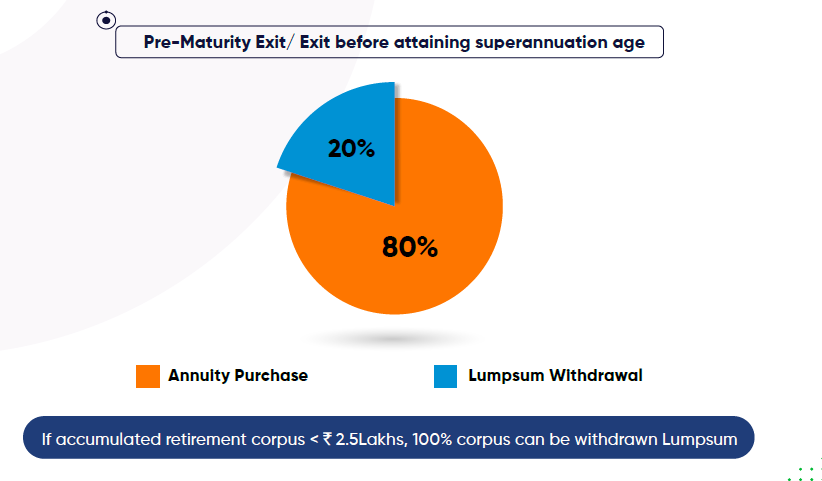

Pre Mature Closure

- The withdrawal treatment varies based on the Subscriber registration, namely, for the Subscriber registration before 60 years and after 60 years.

- For Subscriber Registration Before 60 Years: The Subscriber needs to complete 5 years and has to compulsorily annuitize 80% of the accumulated pension wealth and the remaining 20% can be withdrawn as lump sum. If Corpus <2.50 Lakhs, complete withdrawal is permitted.

- For Subscriber Registration After 60 Years: At the time of withdrawal, if the Subscriber exits after completing 3 years of holding NPS account 60-40 option is available (40% annuity is minimum condition, if the Subscriber wants more pension he can allocate higher annuity percentage). If the Subscriber exits his NPS account before completing 3 years then 20% lumpsum & 80% has to be allocated for annuity option is available.

- In case of death of the Subscriber: Entire accumulated pension fund will be paid to the nominee/s or legal heirs, as per norms. No family pension under the scheme.

Conclusion

Retirement planning may seem tedious but with the right tools, strategies, and a commitment to start early, it can be a reality within your grasp. NPS is a long-term investment, and patience is key. The diverse investment options available through NPS cater to different risk appetites and retirement timelines, ensuring your portfolio aligns with your personal financial goals. By starting early, contributing regularly, and utilizing the scheme's benefits effectively, you can unlock the door to a secure and fulfilling retirement.

Do not wait any longer. Take the first step today by exploring your NPS options, seeking professional financial advice, and charting your course towards a fulfilling and financially secure early retirement.

Quick Take

Q: What is the National Pension Scheme (NPS)?

A: The National Pension Scheme (NPS) is a retirement savings scheme initiated by the Government of India to provide regular income during old age.

Q: How can I join the NPS scheme?

A: To join the NPS scheme, you need to contact a registered service provider and fill out the subscriber registration form.

Q: What are the tax benefits of investing in NPS?

A: Investing in NPS offers tax benefits under Section 80C of the Income Tax Act. Additionally, contributions up to a certain limit are tax-deductible.

Q: Can I open more than one NPS account?

A: You can open multiple NPS accounts, but only one account can be a Tier I account, which is mandatory for contributions.

Q: How does the NPS calculator work?

A: The NPS calculator helps you estimate the future value of your contributions based on factors such as tenure, contribution amount, and expected returns.

Q: What is the Atal Pension Yojana (APY) and how is it related to NPS?

A: The Atal Pension Yojana (APY) is a scheme under the NPS aimed at providing pension benefits to workers in the unorganized sector. Subscribers can contribute towards the APY through their NPS account.

Q: What is the withdrawal process for NPS?

A: NPS subscribers can make partial withdrawals for specific purposes like higher education, buying a house, or medical emergencies. However, a certain portion of the corpus needs to be used to purchase a pension post-retirement.