On Tuesday, 26th of March, Finance Minister Nirmala Sitharaman posted regarding the Atal Pension Yojana where she highlighted the scheme’s proposition of providing a guaranteed pension. She even reminded her followers that the APY has generated record returns of 9.1% since inception. Considering the returns of other savings plans it is a quite decent rate standing in 2024.

Till March 4, nearly 4.53 Crore subscribers have enrolled themselves under this scheme. This tremendous success has been possible only because the administration maintains robust communication channels till every subscriber reaches their retirement. To get further insights on her post, you may continue reading this article.

Ministry of Finance’s Assurance on APY Scheme

The honourable FM justified how the Atal Pension Yojana is based on best practice architecture. She reminded the Indians that the automatically renewing feature of the premium payment had been set deliberately. This is because the Government believes it is in the best interest of the subscribers.

The psychology behind this stance has been stated as: Instead of recommending beneficiaries resume their contributions, this explicit feature forces subscribers to rethink why they want to discontinue. This strenuous decision-making indirectly allows all to save systematically for their retirement.

Further, the inclusion initiative designed by the Central Government allows both public and private banks to extend facilities to the wider population. As a result, those registering just at the age of 18 with only a Rs. 42/month subscription can be assured of getting Rs. 1000 monthly after they retire. Similarly, one can assure a fixed pension of Rs. 5000 per month by increasing their regular contributions.

Moreover, Smt. Nirmala Sitharaman remarked “This is an attractive guaranteed minimum return. GoI pays a subsidy to PFRDA to make up for any shortfall in actual returns. If higher investment returns are received on the contributions of subscribers of APY, the higher pension would be paid to the subscribers. In fact, currently, the returns are more than 8%.”

Now one may wonder how PFRDA manages to compensate for the shortfall in contributions. In this perspective, Sitharaman said that the Government pays a certain subsidy to make up for the deficit. However, even if the cumulative investment generates a greater profit the whole amount is distributed among the beneficiaries.

Unveiling the Past Performance of the Atal Pension Yojana

The Atal Pension Yojana was initiated by the Indian Government on May 9, 2015. As per the latest declarations of the PFRDA, the total assets under management or AUM of APY have been calculated as Rs, 10,00,000 Crores.

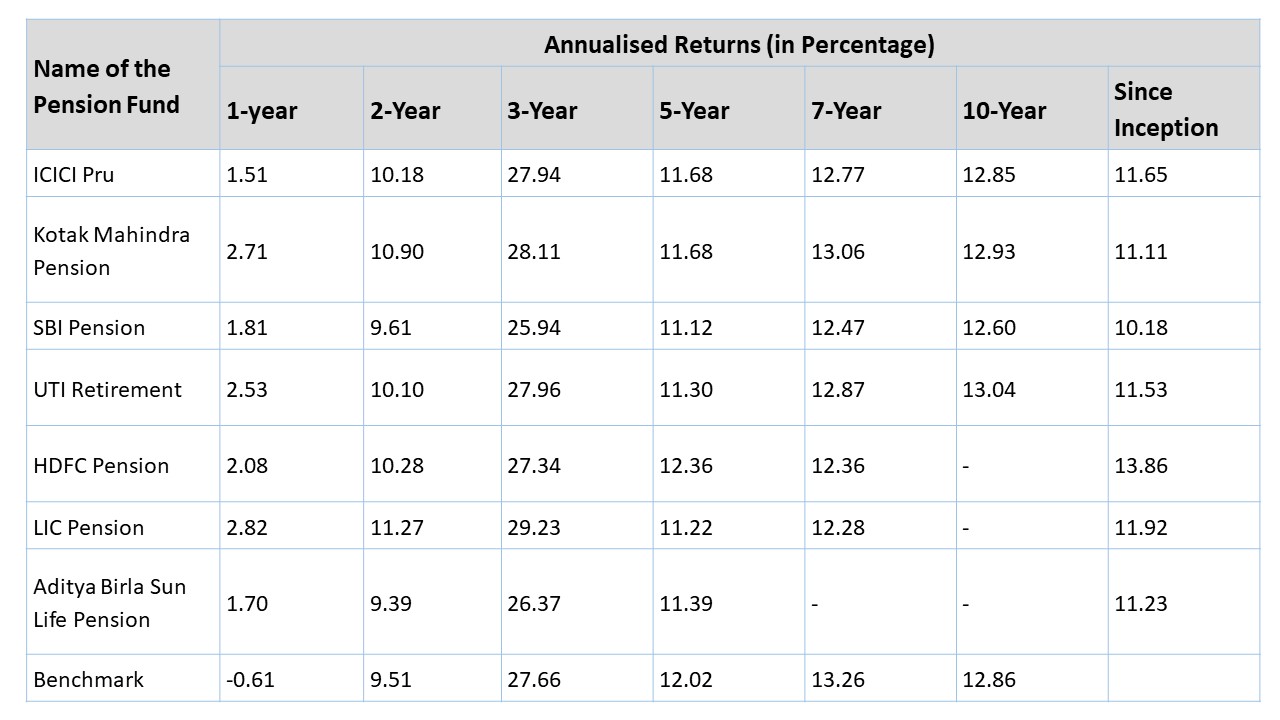

On a further positive note, three new Pension Fund Managers joined this PFRDA-led scheme in 2023. In the following table, you can analyse the annualised returns generated by the previous 7 PFs for the unorganised/private sector Scheme E – Tier I:

Source: NPS Trust.

Please note that the “Benchmark” row has been presented to gauge the performance of APY against the equity market. Also, there are three other PFs namely the Max Life Pension, Tata Pension and Axis Pension schemes respectively. The data of these funds are insufficient for comparison since these are relatively new to the market.

Key Points to Consider Before Joining the APY Scheme

The Atal Pension Yojana is primarily designed to ensure post-retirement financial security for unorganised sector workers.

To get a guaranteed pension under the APY, you must join the scheme while you are between 18 - 40 years old. Also, having a bank account/ post office account will be mandatory for benefitting from this scheme.

Here are some additional points to consider:

- The Indian Government will co-contribute a subscriber’s account for the first five years if they meet certain criteria. For instance, such beneficiaries should not be already enrolled under any other social security schemes. Then, the Government aid appears as 50% of the regular contributions with an upper annual limit of Rs. 1000 per subscriber.

- All investments under APY are as per the guidelines published by PFRDA.

- Beneficiaries can contribute to their accounts as per the half-yearly/ quarterly/ monthly frequency.

- The due date is set by the subscriber themselves which can be any date of a specific month.

- In cases of payment default, banks charge Rs. 1 per Rs. 100 worth of contributions for every delayed monthly contribution.

- You have to bear an annual service charge of Rs. 100 as well as a one-time registration fee while opening the account. The registration charge depends on the volume of subscribers and can go up to a maximum of Rs. 150.

So, in case the specifications are clear, you can proceed towards subscribing for APY by visiting the Protean eGov Technologies Ltd platform.

After filling out the details in the application form and adding nomination information you are prompted to add the initial deposit. The account opening confirmation reaches your registered phone number within 24 hours. Also, you receive a unique Permanent Retirement Account Number (PRAN) that becomes crucial while exiting from the Atal Pension Yojana.

In summary, Nirmala Sitharaman's opinion majorly highlights the key factors of the Atal Pension Yojana. One can embark on its trustable framework and convincingly avoid political criticisms. It is a guaranteed pension plan that is set to offer flexible participation provisions to the subscribers.

- Story by Bruhadeeswaran